How the RFQ System Works

Gryps is not an order-book exchange. It uses an intent-based Request for Quote (RFQ) system to match traders with professional market makers, producing better execution for most trade sizes than a traditional central limit order book.

This page explains what happens when you place a trade on Gryps, why the RFQ model exists, and what makes it different from the order-book DEXs you may be used to.

The core idea

On an order-book exchange like Hyperliquid or dYdX, you submit a specific order (market or limit) into a shared book. Your order sits alongside everyone else's. Execution depends on what liquidity happens to be resting in the book at that moment.

On Gryps, you express a trading intent -- what you want to trade, in what size, with what leverage. That intent is broadcast to a network of professional solvers who compete in a real-time auction to fill it. You get back a firm quote reflecting the best price the auction produced.

The difference matters because it changes *where liquidity comes from*. An order book is limited to the liquidity posted on that specific venue. An RFQ auction lets solvers source liquidity from anywhere -- other perpetual exchanges, spot markets, OTC desks -- and pass the result to you as a single executable quote.

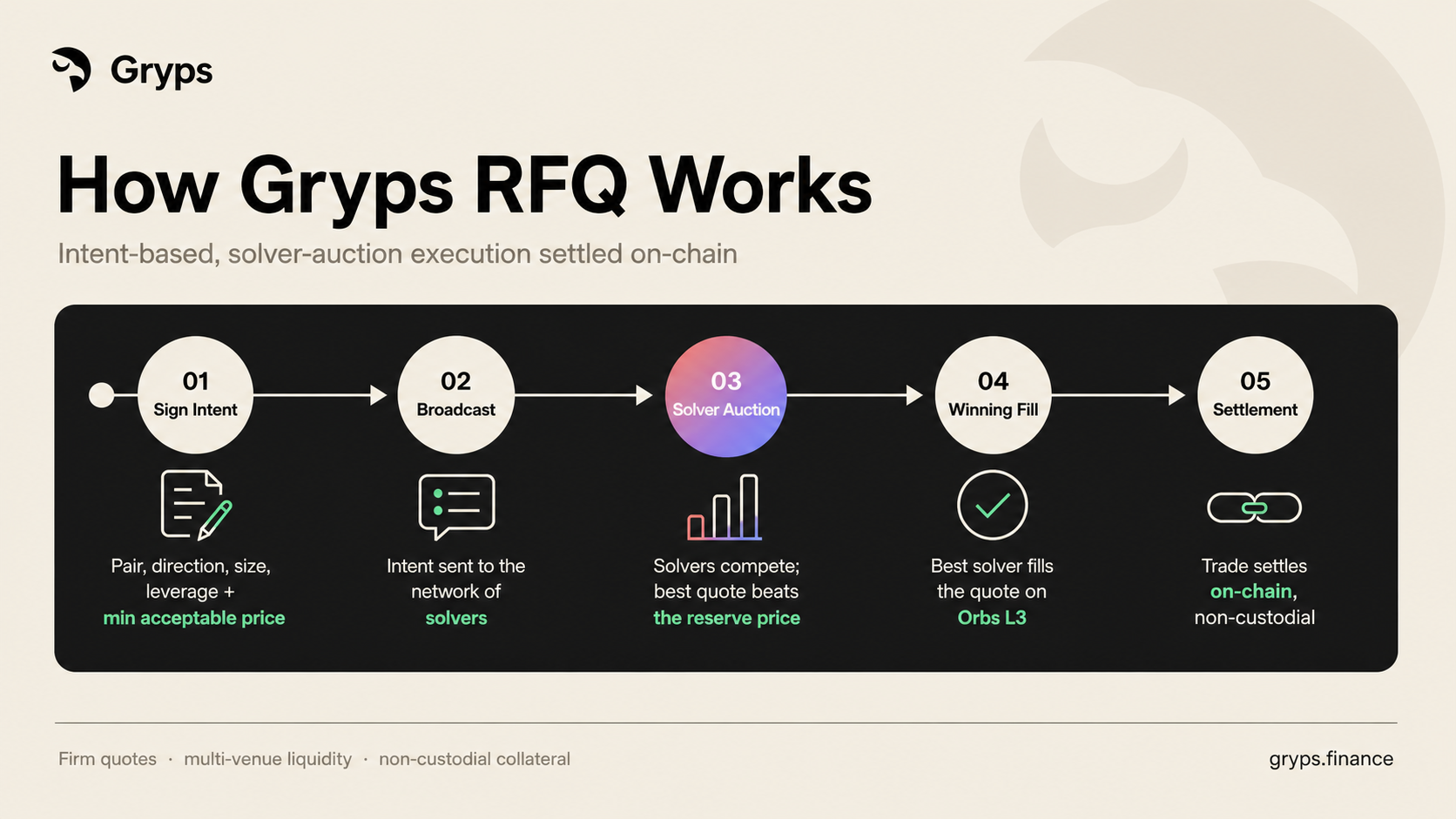

Gryps RFQ flow: intent signing, solver-auction execution, winning fill on Orbs L3, and non-custodial on-chain settlement.

What happens when you trade

1. You submit an intent

You specify the trading pair (e.g., ETH-USDC), direction (long or short), position size, and leverage. This is your trading intent. It describes *what you want*, not a specific order at a specific price.

Your collateral is denominated in USDC.

2. The solver auction runs

Your intent is broadcast to Gryps's solver network, powered by Orbs. Multiple solvers -- also called hedgers -- see your request simultaneously and compete to offer you the best execution price.

This auction typically completes in seconds. Each solver evaluates your intent against its own liquidity sources and risk models, then submits a quote.

3. You receive the best quote

The auction surfaces the most competitive quote. The price you see reflects real-time competition between solvers who are actively sourcing liquidity across multiple venues.

Unlike an AMM, there is no algorithmic pricing curve. Unlike a thin order book, you are not dependent on whatever passive liquidity happens to be resting at that price level. The quote is the product of active competition.

4. On-chain settlement

When you accept the quote, Symmio's smart contracts settle the trade on-chain on SEI. The settlement is bilateral -- a direct contract between you and the specific solver who won the auction.

Your USDC collateral is locked in the smart contract. It is not pooled with other users' funds, not held by Gryps, and not custodied by the solver. The contract enforces the terms of the trade trustlessly.

5. Position management

Your open position exists as an on-chain bilateral agreement. You can:

- Add or remove margin to adjust your liquidation price

- Partially close to take profit on a portion of the position

- Fully close at any time by initiating a new RFQ to exit

All position management actions settle through the same on-chain contract layer.

Why RFQ produces better execution

Tighter spreads through competition

When multiple solvers compete for your order flow, the spread compresses. This is the same dynamic that drives institutional FX and fixed-income markets -- competitive quoting consistently produces tighter spreads than passive order books for most trade sizes.

Deep liquidity without a local order book

Solvers are not limited to liquidity posted on Gryps. They can hedge across centralized exchanges, other DEXs, spot markets, and OTC channels. The effective liquidity available to you is the *aggregate* of every venue the solver network can access, not just what is sitting in one book.

No slippage surprises

On an order-book DEX, a market order executes against whatever resting liquidity exists. If the book is thin, you eat through multiple price levels (slippage). On Gryps, you see a firm quote before you accept it. The price you see is the price you get.

Self-custody throughout

Your collateral is held in Symmio's on-chain smart contracts at all times. There is no intermediary custody layer, no pooled vault that socializes risk, and no centralized counterparty. The bilateral contract structure means your exposure is between you and the solver who filled your trade -- enforced by code, not trust.

Why RFQ matters for larger traders

The RFQ model was designed with institutional-grade flow in mind:

- Block-sized trades -- Solvers can handle positions well into the hundreds of thousands of dollars without moving the market, because they source and hedge across multiple venues simultaneously.

- Execution quality scales with size -- The auction mechanism incentivizes solvers to compete harder for larger orders, since the profit opportunity is greater. This is the opposite of order-book dynamics, where larger orders typically face worse execution.

- No information leakage -- Your intent is broadcast to the solver network, not displayed in a public order book. There is no opportunity for other traders to front-run your order or trade against your visible size.

How solvers work

Solvers (also called hedgers) are professional market makers who connect to Gryps's solver network. Their role in the system:

- 01

Receive intents from the Orbs-powered solver network

- 02

Price the trade using their own models, data feeds, and risk parameters

- 03

Compete in the auction by submitting quotes

- 04

Take the other side of your trade when they win the auction

- 05

Hedge their exposure across other venues to manage risk

Solvers do not take naked directional bets on your trades. They are in the business of capturing the spread between your execution price and their hedge cost. This is the same business model that drives market making on traditional exchanges -- applied to on-chain perpetuals.

The solver network currently includes connections to multiple perpetual venues. Additional venue integrations -- including Hyperliquid for tokenized equity and commodity perpetuals -- are actively being onboarded, which will further deepen the liquidity available through the auction.

RFQ vs. order book vs. AMM: a comparison

| RFQ (Gryps) | Order Book (Hyperliquid, dYdX) | AMM (GMX, GNS) | |

|---|---|---|---|

| Liquidity source | Multi-venue via solver network | Resting orders on a single book | Algorithmic pool |

| Pricing | Competitive auction | Best bid/offer in book | Bonding curve / oracle |

| Slippage | Quote is firm before acceptance | Depends on book depth | Depends on pool depth and trade size |

| Large trade execution | Solvers source across venues | Eats through book levels | High price impact |

| Custody | On-chain bilateral contracts | Varies by implementation | Pool-based |

| Front-running risk | Intent is not publicly visible | Public order book | Oracle manipulation risk |

The infrastructure stack

Gryps's RFQ system is built on two core infrastructure layers:

- Symmio -- The trustless clearing and settlement layer. Symmio's smart contracts handle collateral locking, bilateral agreement enforcement, liquidation logic, and on-chain settlement. This is what makes the system non-custodial and trustless.

- Orbs -- The decentralized solver network layer. Orbs powers the intent broadcast and auction infrastructure that connects your trading intents to the solver network. This is what makes the competitive auction possible without a centralized matching engine.

Together, these layers allow Gryps to offer institutional-grade execution with on-chain settlement and self-custody -- without maintaining its own order book or liquidity pools.

Learn more

- High-Level Architecture -- How Symmio, Orbs, and the solver network fit together at the protocol level

- Getting Started -- Step-by-step walkthrough of connecting, funding, and placing your first trade on Gryps